June Market Update

Checking in on the Construction Pipeline

Greater Fort Worth multifamily performance has been something of a mixed bag so far in 2024. On one hand, rent growth has outpaced last year’s on the back of improved apartment demand. On the other hand, even net absorption considerably better than last year’s has not been enough to offset new supply. Average occupancy has continued its free fall as a result. With new supply set to be a major force this year and next, it’s a good time to check in on the construction pipeline.

Recently Delivered Units

Approximately 6,200 new units were delivered in the first five months of the year. This was 35% higher than in the same portion of 2023 and doubled the five-year average of 3,100 new units from January through May.

Three submarkets have been at the forefront of recent deliveries. About 1,700 new units delivered in the Denton – Corinth region led the way in the period, followed by more than 1,400 new units in North Fort Worth and just over 1,300 new units delivered in Central Fort Worth. Of twelve ALN submarkets for Great Fort Worth, ten have seen at least one new property delivered so far this year.

Of course, the full picture of recent new supply does not only include those properties introduced this year. There remain properties delivered prior to 2024 that continue to move toward stabilization. In total, there were almost 19,000 units in some phase of lease-up at the end of May. These units include projects that are still completing construction but are already leasing as well as properties that have fully completed construction but have not ye stabilized. To add some context to the number of units in this basket, annual net absorption for Greater Fort Worth over the last decade has been about 3,700 units.

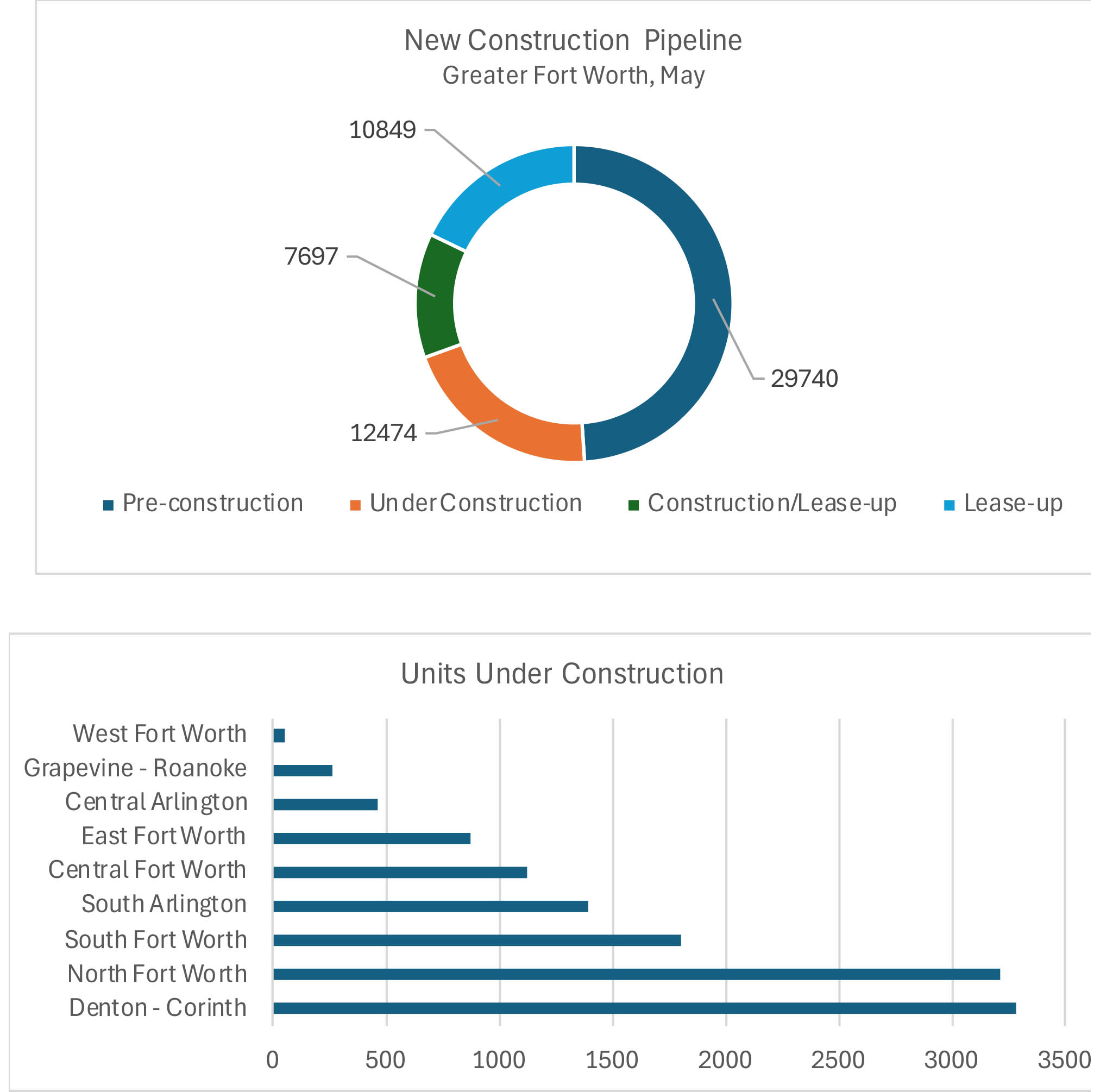

Units Under Construction

In addition to the massive number of units in lease-up, there are nearly 13,000 units currently under construction that have not yet begun to lease. A majority of these units are expected to be in the market by the end of next year and represent the short-term picture for upcoming new supply.

When sorting Greater Fort Worth submarkets according to units under construction, the same areas that have led the way in recent deliveries populate the top of the ranking. This is a bit of a double-edged sword because on the one hand, not every region of the market will be facing supply pressure. On the other hand, a few submarkets will continue to bear the brunt of the supply glut.

In the Denton – Corinth area, there were roughly 3,300 units under construction at the end of May. North Fort Worth was the location of just over 3,200 units under construction, and South Fort Worth rounded out the top three submarkets with approximately 1,800 units. Central Fort Worth, the submarket with the third-most deliveries so far this year, has the fifth-most units under construction with just over 1,100.

Nine submarkets had units under construction at the end of May, not much different from the ten submarket that have already seen new supply this year. To reiterate the point about upcoming new supply being a fairly concentrated phenomenon, more than half of the total units in this phase of the pipeline are located in the top two submarkets.

Takeaways

Apartment demand has rebounded nicely so far this year, but that is not the whole story. Net absorption remains low relative to the pre-pandemic period and net absorption within stabilized properties has been negative through May for the third straight year. The increase in demand has also not come close to offsetting new supply that is peaking at an inopportune time.

Looking ahead to the end of the year, new supply is all but certain to apply further downward pressure on an overall average occupancy that is already lower than at any point during the Great recession period. For stabilized properties, some cushion still remains relative to the trough of that period. Rent growth has remained in positive territory so far this year, but it is certainly possible that 2024 will be the second consecutive year to suffer negative average effective rent growth for new leases.

Jordan Brooks

Senior Market Analyst – ALN Apartment Data

Jordan@alndata.com

www.alndata.com

Jordan Brooks is a Senior Market Analyst at ALN Apartment Data. In addition to speaking at affiliates around the country, Jordan writes ALN’s monthly newsletter analyzing various aspects of industry performance and contributes monthly to multiple multifamily publications. He earned a master’s degree from the University of Texas at Dallas in Business Analytics.